At a simple level, a blockchain is a shared digital record that many people can access and trust, without needing a single central authority like a bank or company to manage it.

In traditional systems, one organization (like a bank) keeps the official record. With blockchain, that responsibility is shared across a network of computers, creating a system that is more open, transparent, and resilient.

A helpful way to think about it: Cryptocurrency is the vehicle, and Blockchain is the engine that makes it run.

A blockchain is often called a distributed ledger, which means:

Information is stored across many computers (called nodes)

Everyone on the network shares the same version of the record

No single party has total control

This design brings a big advantage. There’s no single point of failure . It’s much harder to tamper with records, and it reduces the need to fully trust one central organization.

Because of this, blockchain is gaining traction not just in finance, but also in supply chains, digital identity, contracts, and more.

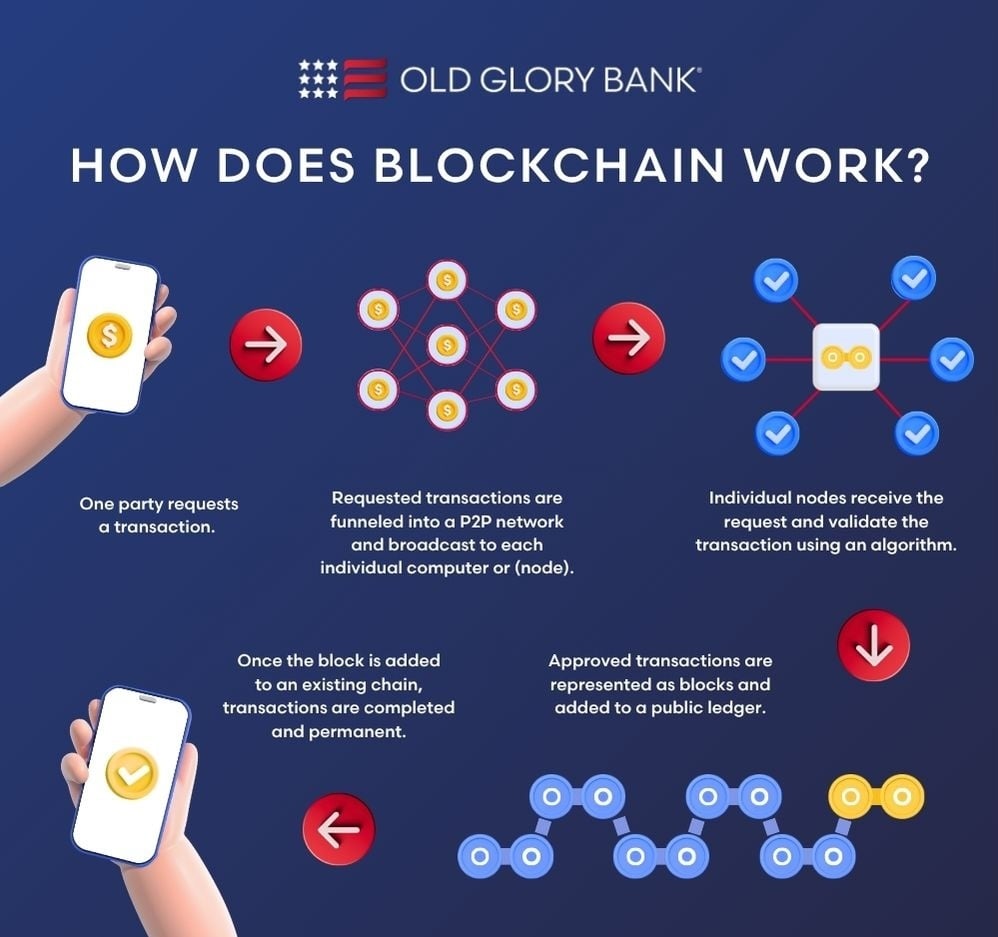

Even though blockchains can differ, most follow a similar process:

You start a transaction. For example, you send crypto to someone or interact with an app.

The network checks it. The system verifies that everything is valid (that you own the funds, or that nothing is being double-spent).

Transactions are grouped into a block. Think of a "block" as a bundle of recent activity.

The network agrees it’s valid (consensus). Participants (validators or miners) confirm the block.

The block is added to the chain. It connects to previous blocks, creating a permanent record.

Once completed, the transaction becomes extremely difficult to change, which helps create trust without needing intermediaries.

Blockchain’s strength comes from three key ideas:

1. Immutability (Hard to Change)

Once information is recorded, it’s incredibly difficult to alter. This creates a reliable, tamper-resistant history.

2. Decentralization (Shared Control)

No single organization controls the system. This can:

Increase resilience

Reduce dependence on middlemen

Give users more direct control

3. Transparency (Open Verification)

Many blockchains allow anyone to verify transactions. This builds accountability and trust, even between strangers. The transaction is verifiable, but the sender and recipient’s identities remain anonymous.

Blockchain offers strong protections, but it’s not “set-it-and-forget-it” secure.

Security depends on:

The network design

The quality of the code

The choices users make

In other words, blockchain improves trust systems , but users still play an important role.

Blockchain doesn’t eliminate risk – it shifts where responsibility lives.

In traditional finance:

Institutions may help recover accounts

Errors can sometimes be reversed

In blockchain systems:

Key responsibilities include:

Managing private keys and passwords.

Losing them can mean losing access permanently.

Understanding the technology. Bugs or weak smart contracts can still exist.

👉 The upside: more control and independence

👉 The tradeoff: more personal responsibility

Blockchain isn’t just for crypto. It can be used anywhere people need a shared, trustworthy record, such as:

Financial systems

Supply chain tracking

Digital contracts (smart contracts)

Identity and ownership records

It’s not the right solution for every problem, but in the right situations, it can increase transparency, efficiency, and trust.

Blockchain represents a shift in how we think about:

Trust (from institutions → networks)

Ownership (more direct control)

Participation (more open systems)

It can empower individuals and organizations to move value more freely, verify information independently, and reduce reliance on intermediaries.

At the same time, success in this space requires education and responsibility.